Payments

Payments

Solutions

Solutions

Industries

Industries

Services

Services

Resources

Resources

.png)

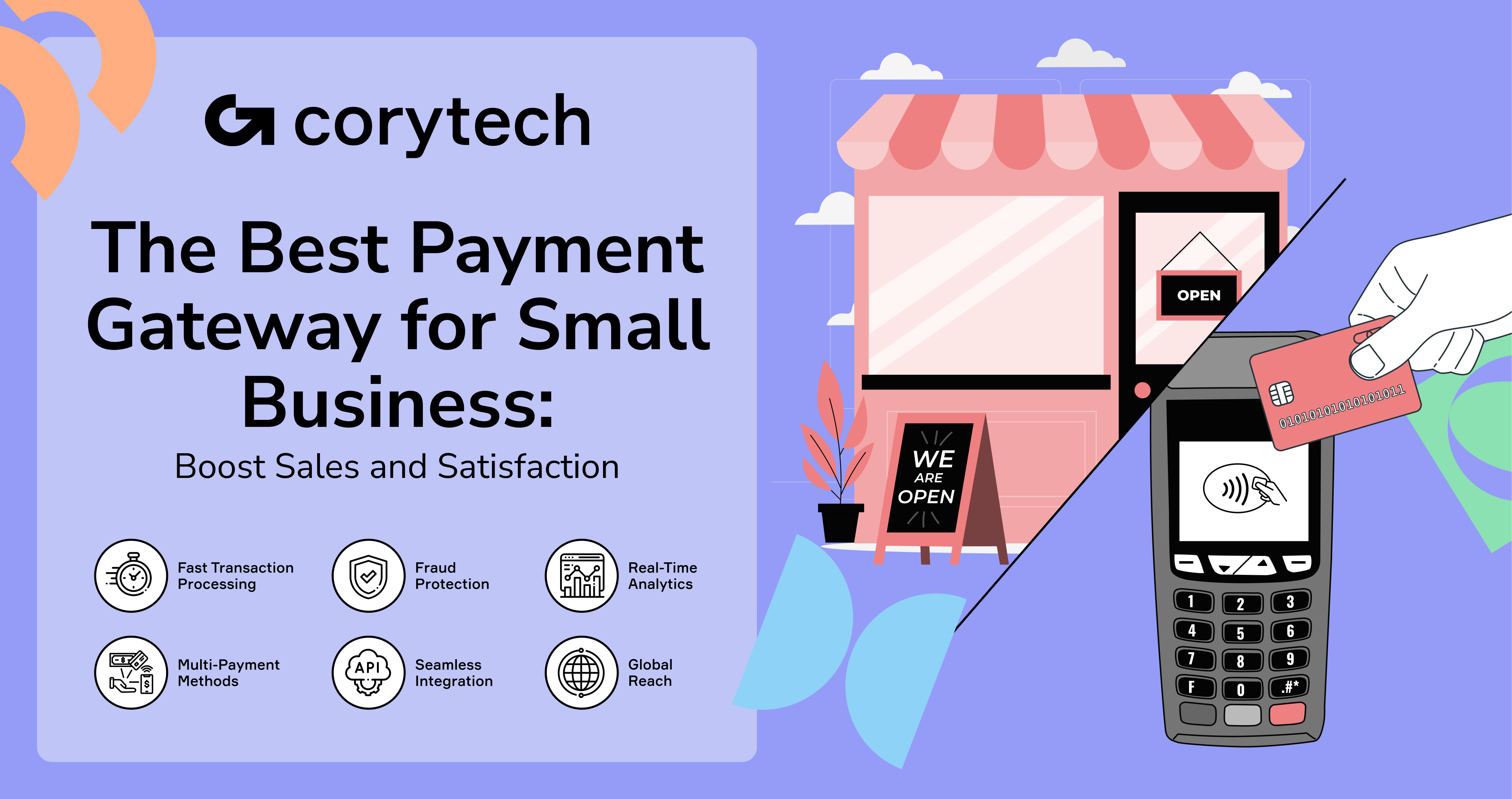

Why “payments” ≠ “plumbing” anymore

Every extra second of lag or line of checkout friction is lost money. A recent Baymard Institute study shows the average cart-abandonment rate still hovers around 70 percent, and hidden costs or slow approvals are prime culprits. Payment processing is the critical business function of moving payments for goods and services between bank accounts.

A modern payment system is now essential infrastructure for small businesses, ensuring seamless, secure, and efficient transactions that support business growth.

Payment processing is important for businesses of all sizes, including small businesses. For 2025-ready leaders, payment processing for small business is no longer back-office plumbing; it’s a front-of-house growth lever. Frame payments as an expansion engine, and the budget conversation shifts from expense to ROI.

Payment Processing 101: What Happens Behind the Swipe/Tap

Even the simplest sale touches at least five actors:

-

Customer → Payment gateway → Acquirer → Card network → Issuer bank → Acquirer → Merchant. During this flow, the payment gateway verifies funds with the customer's bank before authorizing the transaction. The payment processing cycle is broken down into three parts: transaction initiation, authorization, and settlement. Payment processors play an important role in the payment ecosystem by handling the technical aspects of processing credit and debit card transactions. The payment gateway processes payments by securely transmitting payment data between all parties. Once funds are settled, they are transferred to the business account, which is essential for managing company finances. Micro-delays in any hop kill conversions—especially in real-time verticals like iGaming, where session length volatility is measured in seconds. Merchant services encompass these offerings, including payment gateways, POS systems, and transaction management, to support small businesses in handling electronic payments.

Actors & money flow

-

PSP / ISO – one-stop payment gateway for small business onboarding. Payment processors can be categorized into two types: payment service providers (PSPs) and merchant account providers.

-

Card schemes (Visa, Mastercard, etc.) – brand rails + interchange economics.

-

Fraud stack – 3-D Secure, risk scoring, velocity rules.

Pain points unique to SMB PSPs

-

Chargeback spikes when hot streaks cool.

-

Multi-currency volatility (FX swings hit payouts).

-

Session-length + load spikes that expose single-acquirer bottlenecks.

Dealing with chargebacks and disputes can be time-consuming and costly for small businesses.

.png)

The Payment Methods Customers Expect in 2025

Digital wallet usage is exploding: 4.3 billion users in 2024 are forecast to reach 5.8 billion by 2029. The opportunity framing: wallets aren’t an “extra button” but an on-ramp to global audiences. Online payments and online payment methods are essential for e-commerce and remote transactions, offering convenience and flexibility for both businesses and customers. Mobile payments and digital wallet payments are increasingly popular, allowing customers to pay using their preferred payment method, whether in-store or online.

For businesses looking to expand geographically, electronic payment systems allow them to accept payments from anywhere in the world. Fast payment processing means small businesses receive money quickly, improving their ability to manage daily expenses. Offering a variety of payment solutions ensures that customers pay in the way that suits them best, improving satisfaction and conversion rates.

Cards still rule—but BIN routing makes or breaks margin

The average U.S. merchant paid $143 billion in interchange fees in 2023 alone. US businesses paid a record $160.7 billion in processing fees in 2022 to accept over $10 trillion in payments from credit, debit, and prepaid cards. Payment gateways for small businesses typically support all major credit cards, ensuring broad customer acceptance and secure, versatile transaction processing. Routing high-cost BINs to lower-fee networks can shave basis points that drop straight to profit.

Mobile wallets & one-click checkouts

Apple Pay / Google Pay with biometric authentication slash friction and qualify for “tokenised” interchange tiers. These solutions enable secure contactless payments, which are increasingly preferred by customers for their speed and convenience.

Local/alternative & crypto rails for global iGaming tables

PIX in Brazil, UPI in India, and stablecoins (USDT, BTC) let players top up instantly while giving small operators local trust signals.

.png)

Frictionless = Profitable: Turning Checkout UX into a Sales Engine

Every extra form field can cut conversion by up to 35 percent. Optimising approval rates is the cheapest growth hack around. Streamlining payment processes and business processes at checkout can significantly boost conversion rates.

When evaluating checkout UX, it's important to consider how POS systems facilitate in person payments and in person transactions for brick-and-mortar businesses. The ability to accept in person payments efficiently is essential for small businesses operating physical locations.

Fewer form fields, higher win-rate

Strip to essentials (card + email). Autofill and network tokens do the rest.

Multi-currency & local language

33 percent of cross-border shoppers bail when the currency at checkout changes unexpectedly.

Smart routing & cascading rescuing “false declines”

Merchants deploying cascading logic report up to 40 percent higher authorisation rates.

Corytech’s adaptive gateway retries failed transactions across multiple acquirers automatically—critical for small-ticket, high-frequency gaming traffic.

.png)

The Hidden Cost Trap: Avoiding Fees That Eat Your Profits

When it comes to payment processing, the devil is in the details—and the fees. Many small businesses are surprised to discover just how much transaction fees, monthly fees, and setup fees can erode their margins.

For example, every time you accept credit card payments, you’re typically charged a transaction fee that can range from 2.6% + 10¢ to 3.5% + 10¢ per sale, depending on your payment processor and the payment method your customer chooses. Credit card payments often come with higher transaction fees than debit card payments, so understanding your customers’ preferred payment methods can help you manage costs.

Monthly fees are another common expense, with some payment processors charging anywhere from $5 to $50 per month just to maintain your account. Setup fees can also catch you off guard, especially if your business requires a more complex payment processing setup—these can run up to $200 or more.

Recurring payments and international transactions can introduce additional costs, with some payment processors charging higher transaction fees or extra service charges for these features. For example, while Stripe and Square are known for their transparent pricing and lack of hidden fees, others like PayPal may tack on extra charges for recurring payments or cross-border sales.

To avoid falling into the hidden cost trap, always review your payment processor’s pricing structure in detail. Consider your average transaction size and monthly transaction volume to determine which provider offers the most competitive fees for your business model. Look for payment processors that offer transparent pricing, and be wary of those with complex fee schedules or higher transaction fees for certain payment types. By staying vigilant and choosing the right payment processor, you can keep more of your hard-earned profits and avoid unpleasant surprises.

Compliance, Security, and Peace of Mind

Security and compliance aren’t just buzzwords—they’re the foundation of trust in payment processing. As a small business, it’s crucial to partner with payment processors that take payment security seriously and adhere to industry standards like PCI DSS (Payment Card Industry Data Security Standard). Compliance in payment processing means your payment processor uses advanced security measures—such as encryption, firewalls, and strict access controls—to safeguard sensitive payment information, including credit card numbers and expiration dates.

A reputable payment processor will also provide ongoing monitoring and regular system updates to protect your business and your customers from evolving threats. Look for features like two-factor authentication, real-time transaction monitoring, and instant alerts for suspicious activity. These tools help you detect and prevent fraud before it impacts your bottom line.

Some payment processors, such as Authorize.net, go a step further by offering tokenization and end-to-end encryption, ensuring that payment data is never exposed during the transaction process. By choosing a payment processor that prioritizes compliance and security, you not only protect your customers’ payment information but also reduce your risk of costly data breaches and fraud. Ultimately, this peace of mind allows you to focus on growing your business, knowing your payment processing is secure and compliant.

.png)

Troubleshooting 101: What to Do When Payments Go Wrong

Even with the best payment processors, hiccups can happen. Knowing how to troubleshoot payment processing issues quickly is essential for keeping your sales flowing and your customers happy. One of the most common problems is a declined transaction, which can result from insufficient funds, expired credit cards, or incorrect payment details. When this happens, double-check the payment information for accuracy and reach out to the customer to confirm their details and ensure they have sufficient funds in their account.

Technical glitches can also disrupt the payment process. If you encounter payment processing errors, start by checking your payment processor’s status page for any reported outages or system issues. If everything appears normal, contact your payment processor’s support team for assistance—they can help you identify and resolve issues, whether it’s a connectivity problem or a configuration error.

Many payment processors, like Stripe, offer robust troubleshooting resources, including error codes and detailed logs, to help you quickly diagnose and fix payment issues. By staying proactive and familiarizing yourself with your payment processor’s support tools, you can minimize downtime and ensure your customers can continue to pay with ease—whether they’re using credit cards, debit cards, or digital wallets.

How to Choose the Right PSP Partner (Checklist for C-Suite)

Selecting the right payment service provider (PSP) is a strategic decision that can shape your business’s growth and customer experience. Here’s a C-Suite checklist to guide your evaluation:

-

Security and Compliance: Ensure the PSP is PCI DSS compliant and prioritizes payment security to protect sensitive payment data.

-

Fees and Pricing: Scrutinize transaction fees, monthly fees, and any additional charges. Look for transparent pricing and avoid providers with hidden fees.

-

Payment Methods: Confirm support for a wide range of payment methods, including credit cards, debit cards, Apple Pay, Google Pay, and other digital wallets.

-

Integration: Assess how easily the PSP integrates with your website, mobile app, and POS system to streamline the payment process.

-

Customer Support: Evaluate the quality and availability of customer support—24/7 assistance can be a game-changer when issues arise.

-

Scalability: Choose a PSP that can handle increasing transaction volumes and adapt as your business grows.

-

Reputation: Research the PSP’s track record for reliability, security, and customer satisfaction within your industry.

By methodically reviewing these factors, you’ll be better positioned to select a PSP that delivers seamless payment experiences, supports multiple payment options, and helps you manage costs as you scale.

Optimisation Roadmap: From “Set-Up” to “Revenue Multiplier”

Maximizing the value of your payment processing system requires a strategic approach that goes beyond initial setup. Here’s a step-by-step optimization roadmap to help you transform your payment processing from a basic utility into a powerful revenue driver:

-

Setup: Integrate your payment processing system with your existing business tools, ensuring compatibility with your website, POS system, and accounting software.

-

Testing: Rigorously test all payment methods—credit cards, debit cards, digital wallets, and recurring payments—to catch errors before customers do.

-

Launch: Go live and start accepting payments, monitoring the first transactions closely for any issues.

-

Monitoring: Use your payment processor’s analytics and reporting tools to track key metrics like approval rates, transaction fees, and payment failures.

-

Optimization: Continuously refine your payment process by A/B testing checkout flows, optimizing for preferred payment methods, and reducing friction at every step.

-

Scaling: As your business grows, ensure your payment processing system can handle higher transaction volumes and support new payment options, including international payments and mobile transactions.

-

Revenue Multiplier: Leverage advanced features—such as recurring billing, payment links, and in-depth analytics—to boost customer retention and unlock new revenue streams.

By following this roadmap and partnering with payment processors that offer robust optimization tools, you’ll ensure your payment processing system not only runs smoothly but also actively contributes to your business’s growth and profitability.

How to Choose the Right PSP Partner (Checklist for C-Suite)

-

Compliance must-haves

-

PCI DSS Level 1 certification

-

Robust AML / KYC tooling

-

Geo-redundant uptime with ≥ 99.95 % SLA

-

Feature fit

-

Unified dashboard with multi-acquirer view

-

Risk scores + chargeback management

-

Subscription / recurring support

-

Crypto on/off-ramps

-

True Total Cost of Ownership

-

Beyond MDR: dev hours, dispute ops, vendor lock-in, and foreign-exchange spreads.

Small businesses must remain compliant with financial regulations to avoid penalties and legal issues.

.png)

Optimisation Roadmap: From “Set-Up” to “Revenue Multiplier”

Track the four golden KPIs

-

Approval rate – target ≥ 95 %.

-

Chargeback ratio – keep < 0.9 %.

-

Average fee (all-in) – know your blended MDR + FX. To get a true picture of payment processing expenses, businesses should also track monthly cost, monthly fee, monthly subscription fees, subscription fees, and any fixed fee components in addition to transaction fees. Some providers may charge relatively high transaction fees or high transaction fees for certain payment methods, which can significantly impact overall profitability.

-

Time-to-funds – cash-flow lifeline for SMBs.

A/B test your pay-page like ad creatives

Rotate layout, button copy, and wallet order every quarter.

Retention tech

Network tokenisation, stored credentials, and in-game top-ups turn the first payment into a relationship.

Key Takeaways & Next Steps

-

Payments are no longer plumbing—treat them as a profit centre.

-

Offer the payment methods (cards, wallets, APMs, crypto) your 2025 customers already expect.

-

Ruthlessly remove friction: fewer fields, local currency, smart routing.

-

Track approval-rate, not just MDR.