Payments

Payments

Solutions

Solutions

Industries

Industries

Services

Services

Resources

Resources

The way we pay is evolving. Coins and bills are being replaced by taps, scans, and clicks. From street vendors to luxury stores, the world is rapidly embracing digital payment systems. The rise of contactless cards, mobile wallets, and digital banking has fueled a global shift towards cashless economies. Contactless payments, in particular, have gained popularity due to the COVID-19 pandemic, offering a hygienic and efficient payment option.

This article explores the key drivers of this transition, the benefits and challenges it brings, and real-world case studies from countries leading the way. Real-time payments, which allow for immediate fund transfers 24/7, are redefining traditional banking norms and are a key component of this transformation. Additionally, the integration of account-to-account (A2A) payments with open banking is expected to drive their adoption, making transactions faster and more cost-effective. Whether you're a policymaker, a business owner, or a consumer, understanding this transformation is essential.

Advantages of a Cashless Economy

Convenience

Cashless transactions offer unmatched ease. Consumers can pay with a tap of a card or the scan of a phone—no need to carry cash, wait for change, or visit ATMs. Peer-to-peer (P2P) payments further enhance convenience by enabling individuals to transfer money directly to one another via online or mobile platforms. Businesses are increasingly adopting digital payment solutions to meet rising customer expectations for speed, convenience, and security. Online payments simplify everything from bill settlements to ordering groceries, creating a frictionless consumer experience.

Safety and Security

Digital payments significantly reduce the risks of theft, robbery, or loss associated with carrying physical money. Additionally, cashless systems help limit the circulation of counterfeit currency, and transactions can be more easily verified and traced if fraud is suspected. Many digital payment technologies also offer enhanced security features, such as biometric authentication, which help prevent fraud and ensure safer transactions for users.

Better Financial Management

Cashless tools like banking apps and expense trackers provide real-time insights into spending habits. Users can budget more effectively, set savings goals, and receive instant alerts about suspicious activity—making personal financial planning more accessible than ever. Digital wallets, which store multiple payment options and offer advanced security measures, further enhance convenience for users. Machine Learning algorithms also enhance customer experiences by providing personalized payment options based on user behavior, tailoring financial tools to individual needs.

Economic Benefits

A digital payment infrastructure speeds up transaction processing, reducing delays in business operations. Faster payments mean increased productivity and smoother trade, contributing to overall economic growth. By adopting advanced payment technologies, businesses can gain a competitive edge by offering faster, more efficient, and customer-friendly payment experiences. It also reduces the cost of printing, transporting, and storing physical cash. The global mobile payment market is projected to reach $27.81 trillion by 2032, highlighting the immense economic potential of this shift.

Reduction in Black Money and Tax Evasion

Digital transactions leave an auditable trail, making it harder for illicit transactions to go unnoticed. Governments can better track income, enforce taxation, and minimize corruption and money laundering, fostering a more transparent economy.

Concerns and Challenges

Privacy Concerns

Every digital payment creates a data footprint, which can be exploited by corporations or malicious actors. Data breaches and the potential misuse of personal financial information raise serious concerns about surveillance and consumer privacy in a fully cashless system.

Exclusion of the Unbanked Population

In many regions, access to banking services remains limited. Elderly populations, rural communities, and economically disadvantaged individuals may lack the resources or digital literacy required to participate in a cashless economy, risking further marginalization.

Dependence on Technology

A fully digital financial system is vulnerable to cyberattacks, software bugs, and infrastructure outages. System failures can paralyze transactions, leaving consumers and businesses unable to access their money when they need it most.

Transition Costs

Shifting to a cashless economy demands significant investment in technology, cybersecurity, education, and regulatory frameworks. Small businesses especially may struggle with the cost of adopting digital payment infrastructure or meeting compliance standards.

.png)

The Role of Financial Institutions

Financial institutions are at the heart of the digital payments revolution, driving the adoption and evolution of payment technology across the globe. As the backbone of the payments industry, banks and other financial institutions are responsible for building and maintaining secure, reliable payment infrastructure that supports everything from mobile payments and digital wallets to instant payments and central bank digital currencies.

Their role extends far beyond simply processing transactions. Financial institutions are leading the way in integrating advanced digital payment technologies, such as biometric authentication and artificial intelligence, to enhance security and streamline the customer experience. For example, the use of fingerprint and facial recognition in digital wallet apps is making it easier and safer for consumers to make payments using their mobile devices.

In addition to technological advancements, financial institutions are committed to reducing transaction costs and promoting financial inclusion. By offering innovative payment solutions like mobile payments and digital wallets, they enable individuals in underserved communities to access essential financial services. Instant payments and faster cross-border payments are also helping to reduce the cost and complexity of international transactions, making global commerce more accessible for businesses and consumers alike.

Collaboration is another key aspect of the modern payments landscape. Financial institutions are increasingly partnering with third-party providers, such as fintech companies, to develop new digital payment solutions and stay competitive in a rapidly changing market. These partnerships allow banks to leverage the latest technologies and emerging trends, providing customers with a wider range of secure, convenient payment options.

Ultimately, financial institutions play a crucial role in shaping the future of payments. By investing in digital payment technologies, reducing transaction costs, and fostering financial inclusion, they are helping to create a more efficient, secure, and accessible payment system for everyone.

.png)

Regulatory Framework

The regulatory framework surrounding digital payments is rapidly evolving to keep pace with technological advancements and emerging trends in the payments industry. Governments and regulatory bodies worldwide are tasked with the complex challenge of protecting consumers and preventing fraud, while also encouraging innovation and competition in digital payment technologies.

One of the primary focuses of regulators is to ensure that digital payment systems are secure and reliable. This involves developing and enforcing standards for security, authentication, and data protection, which help build consumer trust in digital payment solutions. As payment systems become more sophisticated, incorporating technologies like artificial intelligence and machine learning, regulators must adapt their approaches to address new types of security vulnerabilities and fraud risks.

Promoting financial inclusion is another key objective of regulatory frameworks. By supporting the adoption of mobile payments and digital wallets, regulators can help reduce transaction costs and expand access to financial services for underserved populations. For example, regulations that encourage the use of digital payment technologies can make it easier for individuals in remote or rural areas to participate in the financial system, fostering greater economic participation and opportunity.

Regulatory bodies also play a vital role in ensuring that digital payment systems remain competitive and innovative. By setting clear guidelines and standards, they create an environment where both established financial institutions and new entrants, such as fintech companies, can develop secure and efficient payment solutions. This balance between oversight and innovation is essential for the continued growth and stability of the payments industry.

As digital payments become increasingly central to everyday financial transactions, the regulatory landscape will continue to adapt. Ongoing collaboration between regulators, financial institutions, and technology providers is crucial to ensuring that digital payment systems remain secure, inclusive, and responsive to the needs of consumers and businesses alike.

Case Studies — Countries Embracing the Cashless Trend

Sweden

Sweden is often cited as the world’s most cashless society, with less than 10% of all payments made in cash. Government support, banking infrastructure, and widespread consumer adoption of apps like Swish have helped accelerate this transition. Even churches and street vendors now accept mobile payments. The widespread adoption of mobile payment technology in Sweden has helped businesses build customer loyalty by providing convenient and seamless payment experiences.

China

China has undergone a digital payment revolution. Platforms like Alipay and WeChat Pay dominate everyday transactions, from taxis to supermarkets. Each digital wallet app securely stores users' payment information, facilitates seamless transactions, and often integrates with loyalty and rewards programs to enhance user experience. The state has also introduced a central bank digital currency (e-CNY), further solidifying its push toward a digital economy.

India

India’s cashless journey gained momentum with the 2016 demonetization policy, which removed high-denomination currency from circulation. The Unified Payments Interface (UPI) system rapidly gained popularity, enabling instant bank-to-bank transfers and powering a surge in digital payments across urban and rural areas alike.

In UPI transactions, a payment processor acts as an intermediary between the banks, ensuring secure and efficient transfer of funds.

.png)

The Future — What to Expect

Rise of Cryptocurrencies

Cryptocurrencies like Bitcoin and Ethereum are reshaping how we view money. Although volatile and often debated, they offer decentralized, borderless transactions. Cryptocurrency adoption is rising as businesses and consumers accept them as alternative payment methods due to lower transaction fees and decentralization. Governments are exploring central bank digital currencies (CBDCs) as regulated alternatives to private crypto, signaling broader adoption in future economies. CBDCs are government-backed digital assets designed to function alongside fiat currencies, offering a more stable and regulated digital payment option. Central banks are actively involved in developing and implementing CBDCs to enhance financial inclusion, improve transaction efficiency, and influence regulatory practices.

Advanced Payment Technologies

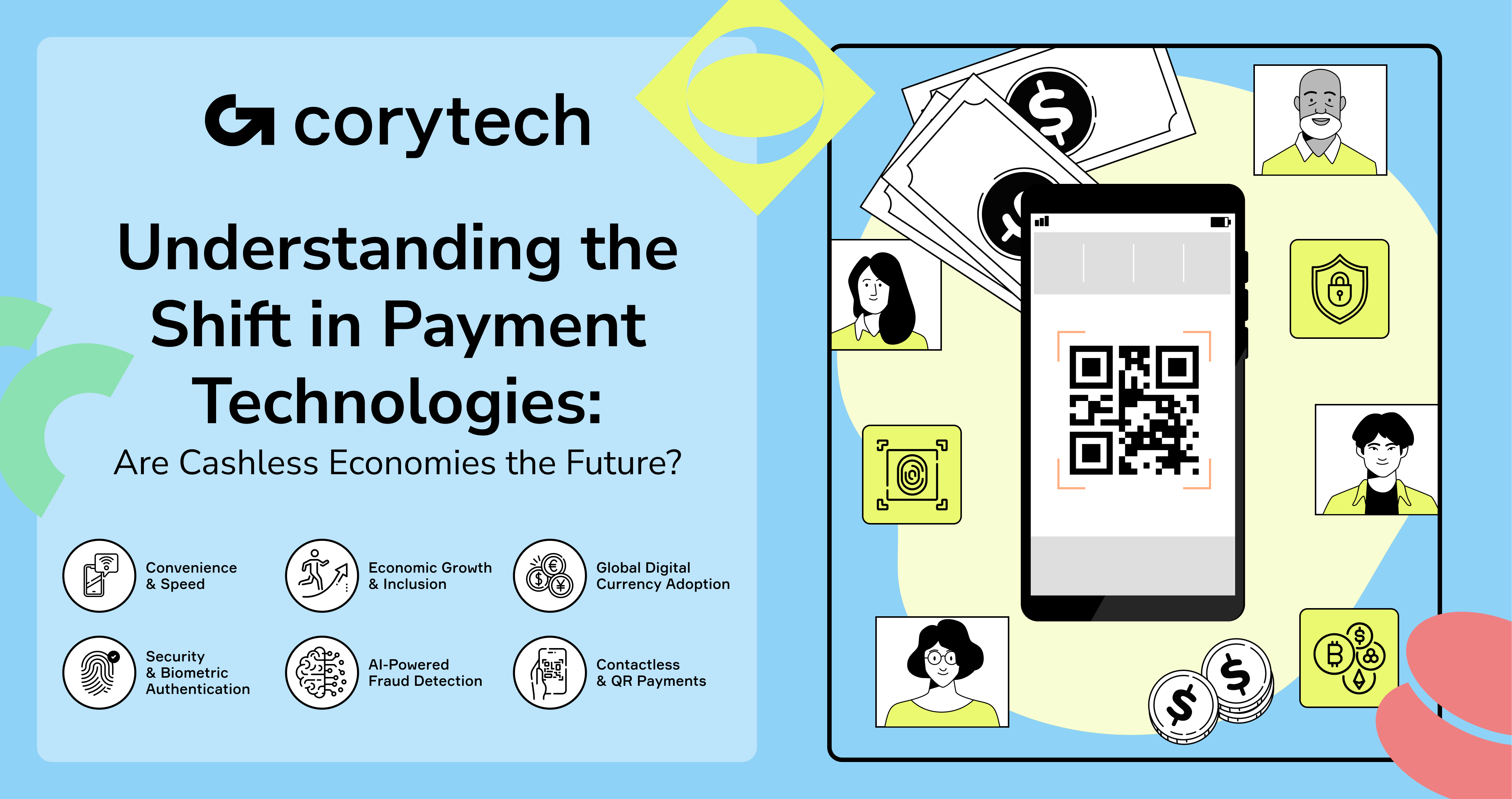

The future of payments is becoming more seamless and secure. Biometric authentication (like fingerprint and facial recognition), near-field communication (NFC), and wearable payment devices are transforming transactions into fast, touchless experiences, enhancing both convenience and security.

NFC-enabled devices communicate securely within close proximity, typically just a few centimeters apart, to facilitate contactless payments. Unlike traditional methods that require physical cards, mobile payments allow users to complete transactions without the need to carry physical cards, offering greater convenience. A mobile device, such as a smartphone or tablet, is used to initiate and confirm transactions, making the payment process quick and efficient.

Biometric authentication is increasingly being integrated into in-store payment systems, such as point-of-sale terminals, to improve speed and security for physical retail transactions. This method offers enhanced security and convenience compared to traditional methods like passwords or PINs.

QR code technology enables fast, secure, and accessible transactions by allowing users to scan or display a QR code for payment. QR code payments are growing in popularity as a digital payment method, offering convenience and security for both merchants and consumers. Merchants across industries are adopting QR codes and integrating them with mobile payment solutions to improve accessibility and reduce transaction costs. Quick response codes facilitate seamless, contactless payments for consumers and merchants. The process of making payments using QR codes can involve either customer-presented or merchant-presented options, streamlining the checkout experience.

Mobile apps play a crucial role in facilitating various digital payments, including digital wallets, bank transfers, and direct carrier billing, enabling convenient and secure transactions across multiple payment technologies.

Artificial Intelligence (AI) is also playing a pivotal role in fraud detection by analyzing transaction patterns and flagging suspicious activities, further bolstering the safety of digital payments.

Artificial Intelligence in Payments

Artificial intelligence (AI) is rapidly transforming the payments industry, offering powerful tools to enhance security, improve the customer experience, and reduce transaction costs. AI-driven payment systems can analyze vast amounts of transaction data in real time, enabling financial institutions to detect and prevent fraudulent activity with unprecedented speed and accuracy. For example, machine learning algorithms can identify unusual transaction patterns and flag potential fraud before it impacts consumers.

Beyond security, AI is also revolutionizing the way customers interact with payment systems. AI-powered chatbots and virtual assistants are now providing instant support for digital payment transactions, helping users resolve issues and complete payments more efficiently. Additionally, AI can personalize payment options and recommendations based on individual consumer behavior, creating a more tailored and satisfying customer experience.

The integration of artificial intelligence into payment systems is also helping to reduce transaction costs by automating administrative tasks and streamlining payment processes. This not only benefits financial institutions by lowering operational costs, but also makes digital payment solutions more affordable and accessible for consumers.

However, the use of AI in payments raises important regulatory and ethical considerations. Regulators must ensure that AI-powered payment systems are transparent, explainable, and free from bias, so that all consumers are treated fairly. Security remains a top priority, as AI systems must be robust enough to withstand evolving threats and protect sensitive payment information.

As AI continues to advance, its role in the payments industry will only grow, offering new opportunities for innovation while also presenting new challenges. By harnessing the power of artificial intelligence responsibly, the payments industry can deliver more secure, efficient, and customer-centric digital payment solutions for the future.

Global Shifts and Policy Changes

As cashless systems expand, we can expect global efforts to standardize digital payment protocols, improve cybersecurity, and ensure inclusion. International cooperation among governments and tech firms will be crucial to managing regulatory frameworks and ensuring equitable access to digital financial tools. Additionally, digital payment systems and CBDCs are reducing reliance on traditional intermediaries, enabling faster and more streamlined transactions.

.png)

What’s Next?

The momentum toward a cashless economy is undeniable. It promises speed, security, and innovation—but also raises critical questions about equity, privacy, and infrastructure resilience. As more countries embrace digital payments, the challenge lies in making this transformation inclusive and secure.

While physical cash may not disappear overnight, its role is shrinking. The future of money is digital—and now is the time to shape what that future looks like.