Payments

Payments

Solutions

Solutions

Industries

Industries

Services

Services

Resources

Resources

.png)

Digital wallets are no longer a feature—they’re the launchpad for your next revenue curve. Consumer demand is a key driver for the adoption of innovations in payment systems and the rapid growth of digital wallets. As innovations in payment technologies reshape how we engage, convert, and retain customers, your digital wallet strategy becomes a core lever for business expansion—not just convenience. The digital payments market is projected to reach $19.89 trillion USD by 2026, underscoring the immense growth potential in this space.

The Paradigm Shift: Wallets as Expansion Engines

From Utility to Growth Lever

Forget everything you thought about digital wallets being a “nice-to-have.” Today, wallets sit at the center of your growth strategy. By offering multiple payment options within digital wallets, you can significantly enhance the customer experience and increase value for both users and businesses.

By embedding frictionless payment experiences directly into user flows, you shift customer acquisition costs (CAC) earlier in the journey while increasing post-purchase lifetime value. The wallet isn’t just a transaction tool—it’s your engine for scaling profitably in a competitive ecosystem. The total transaction value in the digital payments market is expected to reach $11.55 trillion in 2024, highlighting the critical role of digital wallets in driving this growth.

Market Momentum

Gamers, Gen Z spenders, and cross-border shoppers are flocking to seamless digital payment options. The rapid growth of e-commerce, driven by major players and digital innovations, is accelerating the adoption of digital wallets and enabling seamless payment experiences for online shoppers.

If you’re not optimizing for wallet-first experiences, you’re already behind—and your competitors are capitalizing. A 2024 survey revealed that a majority of consumers already use mobile wallets regularly, with 59% reporting use in the last 90 days, emphasizing the growing reliance on these tools.

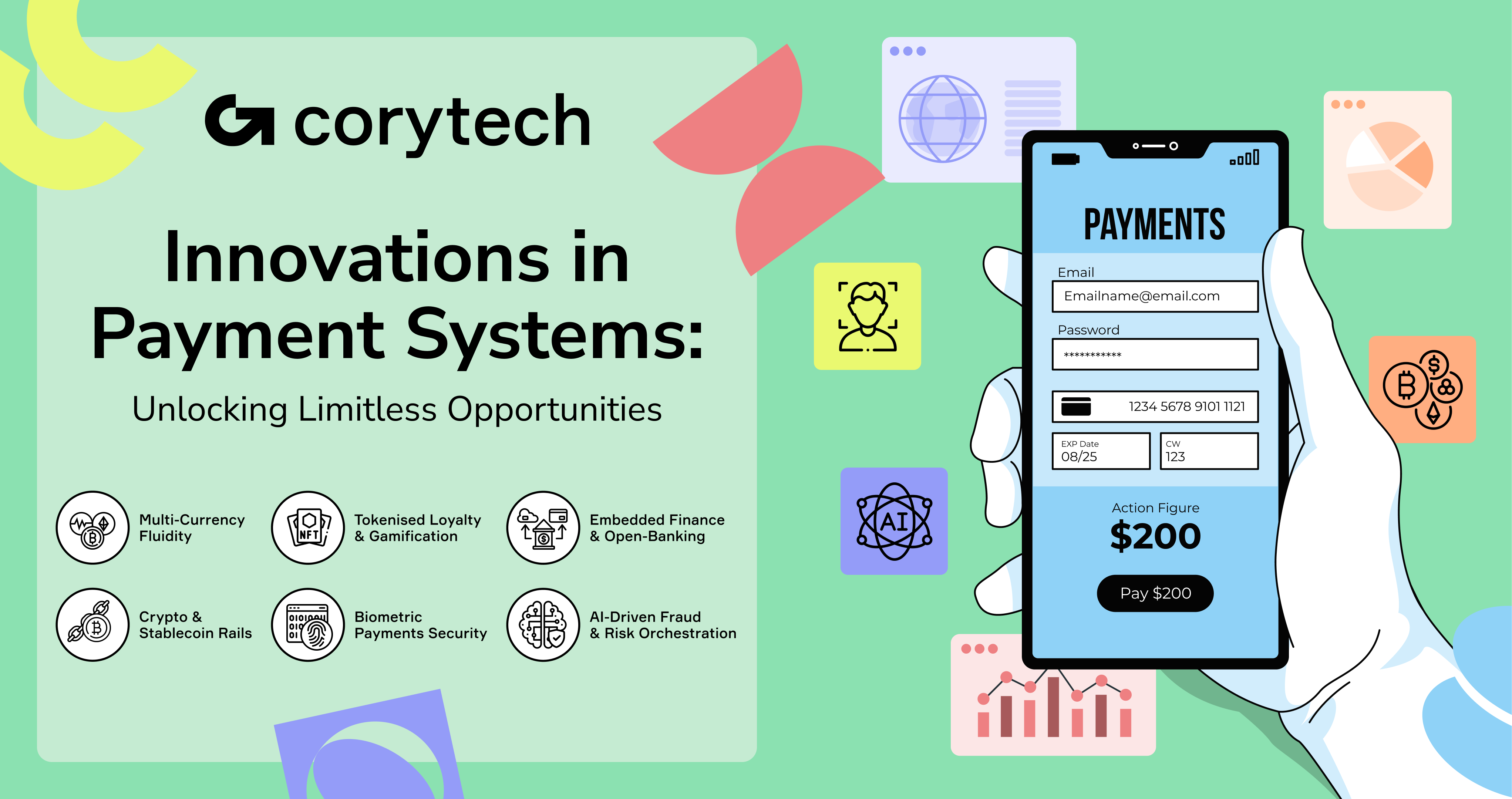

Innovation Pillar #1 — Multi‑Currency Fluidity & Real‑Time FX

Fragmented Rails, Lost Margins

For PSPs and iGaming businesses, managing multi-currency flows often means navigating a maze of regional payment rails, FX delays, and treasury inefficiencies. Traditionally, financial institutions have played a central role in cross-border payments, requiring the sharing of bank account details for transaction verification and approval, which adds complexity and potential delays to the process.

Every currency conversion introduces lag, cost, and risk—eating into margins and throttling your global ambitions. Modern fintech solutions reduce the need to share sensitive bank account details, streamlining cross-border payments and making them faster, cheaper, and simpler, offering a way to overcome these challenges.

Real-Time, Intelligent Currency Management

Imagine one wallet, one unified ledger, and FX that works as fast as your users click. Corytech’s multi-currency wallet solves the chaos with real-time, low-spread conversions and automated treasury logic. Innovations in payment systems are simplifying transferring money across borders, making transactions faster and more secure. Payments providers play a crucial role in enabling real-time, efficient transfers for global businesses. By integrating these innovations, Corytech lets you handle payouts, deposits, and transfers in any currency—without losing control or profitability.

Multi-currency fluidity is no longer a premium feature—it’s table stakes for scaling into new markets with confidence.

Innovation Pillar #2 — Crypto & Stablecoin Rails

Speed, Privacy & Profitability

In high-stakes, high-volume environments like iGaming, milliseconds and margins matter. Crypto and stablecoin payment rails aren’t just buzzwords—they unlock 24/7 settlement, greater player anonymity, and dramatically reduced transaction fees. For digital-first operators, they’re a gateway to the next tier of competitive advantage.

Additionally, crypto and stablecoin payment rails can drive financial inclusion and economic growth in developing economies by providing accessible and efficient digital payment services.

Smart Execution: Beyond the Hype

But innovation without precision can backfire. To truly leverage crypto in your digital wallet strategy, you’ll need to navigate critical choices:

- Custodial vs. Non-Custodial: Control vs. user sovereignty

- On-Ramp/Off-Ramp Orchestration: Seamless conversion and liquidity access

- AML & Compliance Overlays: Embedded, not bolted-on, to meet evolving standards

Ensuring regulatory compliance and adherence to industry security standards is essential for legal operation, security, and smooth integration with financial institutions when implementing crypto payment solutions.

Corytech’s infrastructure supports compliant, scalable crypto flows—positioning you to embrace the future without tripping regulatory wires.

Crypto isn’t about speculation—it’s about strengthening the core mechanics of your payment stack.

Innovation Pillar #3 — Embedded Finance & Open‑Banking Pay‑by‑Bank

Streamlined Journeys, Amplified Outcomes

What if your checkout process disappeared altogether? Embedded finance—powered by open banking—makes it possible. Essential components of modern embedded finance solutions include features like pay bills, bill payments, and debit card integration, which streamline digital wallet experiences and enhance user convenience.

By collapsing traditional payment steps and enabling features like Pay‑by‑Bank, Buy Now Pay Later (BNPL), and instant payouts, businesses can turn clunky conversions into seamless financial experiences. The pandemic ignited the need for BNPL, accelerating its adoption much faster than anticipated.

Better Margins, Smarter Monetization

Fewer steps mean fewer drop-offs. With embedded financial tools, players get what they want faster, and you gain more:

- Higher ARPU (Average Revenue Per User) through upsells like micro-credit

- Fewer Chargebacks via verified, secure account-based payments

- Increased Trust thanks to regulated open-banking infrastructure

Peer to peer payments are another strategic feature enabled by embedded finance, supporting seamless person-to-person transactions.

Corytech’s embedded finance modules make this not just possible—but profitable.

This isn’t just about smoother UX. It’s about re-engineering revenue with innovations in payment technologies.

.png)

Innovation Pillar #4 — Tokenised Loyalty & Gamification

Make Rewards Tangible

Digital wallets can now do more than just store money—they can store value. By embedding tokenised rewards—like NFTs, points, or custom tokens convertible to free bets or spins—you create a system that drives repeat engagement and emotional buy-in. Transaction history helps users track their rewards and engagement, further enhancing the value of digital wallets.

Corytech’s wallet infrastructure is planned to support these gamified elements natively, turning every transaction into a loyalty loop. E-wallets are also becoming more versatile, connecting not only fintech-savvy users but also underbanked communities in developing markets.

Give Ownership, Create Loyalty

This is where behavioral economics meets payment innovation. The Endowment Effect—a cognitive bias where people overvalue things they “own”—means players become more attached to their wallets when they’re filled with personalized, token-based assets. That’s not just retention. That’s investment.

Tokenisation isn’t fluff—it’s a strategic engagement layer grounded in proven human behavior.

Innovation Pillar #5 — AI‑Driven Fraud & Risk Orchestration

Faster, Smarter Fraud

From bot farms hijacking promotions to synthetic identities slipping through KYC filters, the fraud landscape is evolving faster than ever. iGaming and fintech operators face rising losses—not just in revenue, but in customer trust.

Intelligence at the Core

Corytech integrates real-time risk scoring and behavioral biometrics directly into its fraud orchestration stack. This isn’t just monitoring—this is prediction. By learning from every interaction and layering contextual insights, the system can detect suspicious behaviors before they become costly events. AI and machine learning are pivotal in detecting and preventing fraud in payment transactions, ensuring a proactive approach to security.

Think of it as a neural network for your wallet strategy—always watching, always adapting, always protecting.

Fighting fraud used to be defensive. Now, it’s your offensive advantage.

For more in-depth information on AI-driven fraud prevention in fintech, check out our detailed blog post.

Innovation Pillar #6 — Central Bank Digital Currencies: The Next Frontier

Central Bank Digital Currencies (CBDCs) are rapidly emerging as a game-changer in the digital payments ecosystem. By offering a digital version of a country’s fiat currency, CBDCs promise to deliver secure, efficient, and transparent financial transactions that can reshape how businesses and consumers interact. For businesses operating across borders, CBDCs unlock the potential for real time payments, streamlining cross border payments and reducing the friction and costs associated with traditional currency exchange.

This innovation is especially crucial for driving financial inclusion, as CBDCs can extend digital payment access to unbanked populations and reduce fraud risks through traceable, tamper-proof transactions. As the payments landscape evolves, CBDCs are poised to play a crucial role in making global commerce more accessible and trustworthy.

CBDCs: Bridging Trust and Innovation

Central banks around the world are actively exploring and piloting CBDCs, signaling a new era for the payments industry. The Bank of England, for example, is evaluating the introduction of a digital pound, while the European Central Bank is investigating the digital euro’s potential. These initiatives are set to transform the way payments are processed, making them faster, more cost-efficient, and inherently more secure.

With every transaction recorded on a digital ledger, CBDCs offer a powerful tool for central banks to combat fraud and money laundering, while also increasing transparency and trust in the payments system. As more central banks move from exploration to implementation, the payments industry will see a fundamental shift in how value is transferred and safeguarded.

Strategic Implications for Wallet Providers

For digital wallet providers, the rise of CBDCs is both a challenge and an opportunity. On one hand, integrating CBDCs can elevate the security and efficiency of digital wallet transactions, making digital wallets even more appealing to consumers seeking reliable payment solutions. On the other, the direct involvement of central banks in digital payments could disrupt established business models, as consumers may gravitate toward CBDC-native wallets.

To stay ahead, digital wallet providers must proactively adapt—by collaborating with central banks, investing in blockchain technology, and developing innovative payment solutions that harness the unique benefits of CBDCs. The future belongs to those who can seamlessly blend CBDCs into their digital wallet offerings, ensuring their platforms remain at the forefront of the payments revolution.

Innovation Pillar #7 — Biometric Payments & Next-Gen Security

Biometric payments are redefining what it means to make payments securely and conveniently in the digital age. By leveraging technologies like facial recognition and fingerprint scanning, consumers can authorize transactions with a simple glance or touch—no more fumbling for cards, cash, or passwords. As the payments industry continues to innovate, biometric payments are taking on a crucial role in reducing fraud risks and elevating the consumer experience. For businesses, adopting biometric payment methods is not just about keeping up with trends—it’s about delivering the seamless, secure payment experiences today’s consumers demand.

Frictionless Authentication: The New Standard

Biometric authentication is quickly becoming the gold standard for secure payments, offering a frictionless experience that eliminates the need for traditional credentials. Powered by advanced machine learning and artificial intelligence, biometric authentication can detect and prevent fraud in real time, ensuring that only authorized users can make payments.

This not only protects user data but also streamlines the payment process, enhancing customer satisfaction. To maintain robust security, businesses must invest in cutting-edge technologies like near field communication (NFC), tokenization, and encrypted field communication, safeguarding sensitive financial information at every step.

As biometric payments gain traction, businesses that prioritize biometric authentication and data protection will set themselves apart in a crowded market—delivering both peace of mind and a superior user experience to their consumers.

.png)

Future Glimpse — Wallet 3.0 & Programmable Money

The digital wallet of tomorrow will not just hold value—it will enforce logic. As CBDCs (Central Bank Digital Currencies), smart contracts, and context-aware spending rules come online, we’re entering the age of programmable money. A Central Bank Digital Currency (CBDC) is essentially a digital version of a country’s currency, offering new possibilities for financial innovation.

Imagine:

- Instant tax-adjusted payouts for cross-border play

- Smart-contract winnings released only when KYC is confirmed

- Dynamic deposit limits based on real-time risk scoring

In the future, smart home devices, mobile devices such as smartphones and tablets, and other connected technologies will play a key role in making payments. These devices will enable seamless, convenient transactions as part of the broader connected commerce and IoT ecosystem, offering new value for both consumers and merchants.

These aren’t sci-fi ideas—they’re signals. The foundations you lay today determine how ready you’ll be when Wallet 3.0 becomes table stakes.

Your wallet strategy isn’t about catching up. It’s about being first.

Closing Rally Cry

The digital wallet is no longer just a container—it’s your growth operating system. It touches every KPI that matters: acquisition, retention, revenue, and trust. But to unlock its full potential, you need partners who don’t just integrate features—they build for scale. The digital wallet market is increasingly competitive due to easy access to development tools and technological advancements, making innovation a necessity.

Leading digital wallet solutions like Apple Pay and Google Pay exemplify how open-loop wallets can deliver seamless, secure, and cross-platform payment experiences for users and merchants.

At Corytech, we don’t believe in patchwork payments. We build ecosystems. Payments providers play a crucial role in shaping these ecosystems, leveraging digital innovations and payment solutions to enhance the cross-border payments experience and drive transformation across the financial sector.